$1.9M purchase · 14% cap rate

We’re acquiring a stabilized, cash-flowing asset at a 14% cap rate with $391K in verified trailing revenue — underwritten entirely from actuals.

- Underwritten from actuals, not projections

- 89% occupancy — demand validated

- 4.95-star rating across 600+ reviews

19.4% IRR · 3.45× MOIC

We’re raising $650K in investor equity, targeting outsized risk-adjusted returns over a 10-year hold with a refinance event in Year 3.

- 19.4% investor IRR · 3.45× multiple on invested capital

- Year 3 refinance returns $136K to investors

- 58% direct bookings today — targeting 80%

- Clear path to $544K stabilized revenue

Competitive advantage baked into the land

The property sits on 8.14 wooded acres with two structural moats that competitors simply cannot replicate.

- National Forest boundary — no new development on that side, ever

- Private lake easement — exclusive guest amenity access

- 45 min from The Woodlands — one of the wealthiest communities in the U.S.

- 8.14 acres of protected, wooded seclusion

Lake Conroe — accessible via private easement from the property

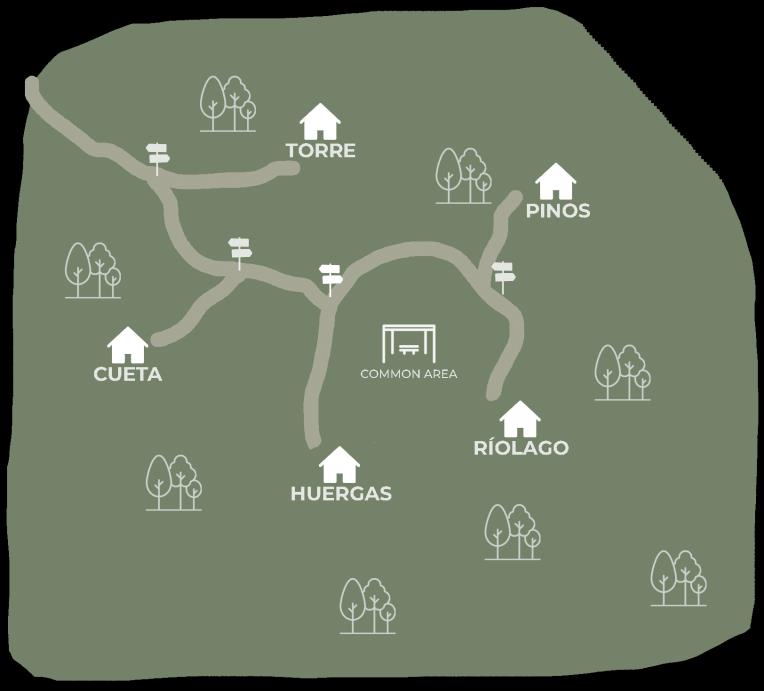

Five architect-designed A-frame cabins on 8 wooded acres

Stay in Babia is a luxury glamping resort featuring five custom-built A-frame cabins — Cueta, Pinos, Riolago, Torre, and Huergas — each named after villages in the Babia region of northern Spain.

Every cabin includes a full kitchen, private bathroom, wood-burning stove, vaulted living room, private deck, and modern finishes throughout. The property also features a communal fire pit area, hammock groves, and direct access to the Lone Star Hiking Trail.

Montgomery, Texas

Located in Montgomery County — one of the fastest-growing counties in Texas — the property sits at the intersection of nature and demand. Sam Houston National Forest borders the property, providing 163,000 acres of protected woodland and the 128-mile Lone Star Hiking Trail.

The site is 60 minutes from downtown Houston (pop. 7M+), 45 minutes from The Woodlands, and within the broader Houston-Conroe growth corridor. Lake Conroe is minutes away.

A growth corridor with structural demand tailwinds.

Montgomery County added 30,000 residents last year alone, and the property draws from Houston metro weekend demand, Woodlands affluence, and a broader structural shift toward experiential travel.

Demand drivers

The Lake Conroe corridor benefits from multiple overlapping demand sources that feed it year-round.

- 7.3M Houston metro — largest weekend feeder market in Texas

- The Woodlands — $141K median HHI, 44% earning $200K+

- Lake Conroe — year-round water recreation destination

- Sam Houston National Forest — 163K acres, 128-mile trail system

Growth trajectory

Montgomery County ranks in the top 10 nationally by population growth, and the trajectory is accelerating.

- 781K residents — 3.9% 5-year CAGR

- +30,000 new residents in the last year alone

- Conroe-Woodlands corridor is a primary growth axis

Industry tailwinds

The broader outdoor hospitality sector is booming as travelers continue shifting from traditional hotels to experiential stays.

- Glamping: $3.45B → $7.9B by 2030 (10.3% CAGR; A-frames +15.6%/yr)

- Boutique hotels: $25B → $40B by 2030 (7.1% CAGR)

- 62% of travelers now prefer experiential over traditional lodging

- Micro resorts offer hotel-grade returns at a fraction of the capital

Sources: U.S. Census Bureau (2025), World Population Review, Grand View Research, SkyQuest Technology, Boutique Hotel Market Report (2024).

Averaging $31K/month at 89% occupancy — with no professional management in place.

This is what the property does today with no revenue management, no dynamic pricing, no direct booking strategy. It’s been operating since March 2024. Trailing 12 months below.

Monthly Revenue (Nov 2024 – Oct 2025)

Monthly Occupancy (Nov 2024 – Oct 2025)

Source: Lodgify PMS. Monthly bars reflect revenue net of platform commissions; the $391,134 trailing-12-month figure is stated gross of platform fees (the basis used for per-cabin revenue and the going-in cap rate). The owner currently lists every cabin at a flat $206/night with no weekend, seasonal, or holiday pricing — effective ADR of $240 is gross booking revenue divided by occupied cabin-nights. Full 20-month history available in the Appendix.

Premium glamping supply is thin. The gap between Babia today and the top of market is the opportunity.

There are very few true comps in the Lake Conroe corridor — purpose-built glamping with professional management. Here’s how Babia stacks up.

| Stay in Babia Current |

Cameron Ranch Coldspring, TX · 46 mi |

Artesian Lakes Montgomery, TX · 12 mi |

Getaway Houston 45 mi |

Babia Target Post-Renovation |

|

|---|---|---|---|---|---|

| Units | 5 | 5 | 8 | 40 | 5 |

| Unit Size | 544 SF | ~221 SF | — | ~160 SF | 544 SF |

| ADR (Weekday) | $206 | $449 | — | $199 | $304 |

| ADR (Weekend) | $206 | $499 | — | $199 | $304 |

| ADR (Blended) | $206 | $297 | $275 | $199 | $304 |

| Guest Rating | 4.95 ☆ | 4.9 ☆ | 4.9 ☆ | 4.7 ☆ | 4.9+ ☆ |

| $/SF/Night | $0.38 | $1.34–$2.26 | — | $1.24 | $0.56 |

| Amenities | Hot tub, picnic tables, lake access | Sauna, hot tub, outdoor bath, experience packages | Small spring-fed lake | None | Sauna, plunge, hot tub, natural pool, kayak rentals, kiosk, lake access |

| Rev / Unit | $78K | $89K | — | — | $109K |

Sources: AirDNA, Google Hotels, Airbnb, operator websites. Cameron Ranch publishes weekday rates of $449 and weekend rates of $499 for ~221 SF units — less than half the size of Babia’s 544 SF cabins. Even their blended ADR of $297 is within range of Babia’s $304 target, which prices at $0.56/SF vs. Cameron Ranch’s $1.34–$2.26/SF. Babia’s $206 is the owner’s flat advertised rate (no dynamic pricing); including cleaning and other guest fees, trailing-12-month revenue is ~$78K per cabin (gross, per Lodgify PMS) — an effective ADR of ~$240.

Moat: irreplicable location

The property borders a national forest and holds a private lake easement. There’s no adjacent land available for development — a structural barrier to entry that only strengthens over time.

Advantage: superior product

Each cabin is a 544 SF architect-designed A-frame with a full kitchen, wood stove, and private deck. Comparable operators charge $297+ for units that are half the size.

Advantage: compounding reviews

A 4.95-star rating across 600+ reviews can’t be bought or replicated overnight. It drives OTA ranking, bookings, and pricing power — and every new entrant starts at zero.

Great product. Run like a side project. That gap is the entire thesis.

The property runs at near-full occupancy despite zero revenue optimization. There are three clear levers we can pull starting on day one.

Pricing: leaving money on every booking

The current owner lists every cabin at a flat $206/night — no weekend premiums, no holiday pricing, no seasonal adjustments. Comparable operators generate 30–50% higher rates with basic dynamic pricing. The listing photos were shot on a phone. All of this is fixable on day one.

Amenities: underdeveloped property

The cabins themselves are beautiful, but the property around them is bare — no outdoor amenities, no communal spaces, no guest experiences. Premium operators in this corridor charge $300+ ADR largely because of amenities this property doesn’t have yet.

Ancillary: untapped revenue streams

The property has a private lake easement and borders a national forest, but neither is monetized. There are no kayak rentals, no firewood bundles, no welcome packages, and no retail — all proven revenue streams that comparable operators already run profitably.

Post-renovation rendering — expanded deck, cold plunge, fire pit seating

From $391K to $544K revenue through operations and capital improvements.

The business plan centers on optimizing what already works through both operational improvements and strategic capital investment — not speculative expansion.

A wellness-forward forest retreat

A $442K renovation transforms what’s already a comfortable stay into a true destination experience.

- Private sauna and cold plunge at every cabin

- Expanded deck with fire pit seating

- Pergola and outdoor living spaces

- Nordic spa add-on packages

- Community self-service kiosk and retail

Target ADR moves from $206 to $304 — validated by Cameron Ranch Glamping, which charges $449–$499/night for units less than half the size.

Natural pool & water features

A chemical-free natural pool that serves as both a landscape centerpiece and a bookable amenity.

- Differentiates from every competitor in the corridor

- Drives premium ADR and longer stays

- Year-round visual appeal for listing photos and social content

- Pairs with sauna and cold plunge for a full wellness circuit

Lake access & outdoor experiences

The property holds a private easement to Lake Conroe that was never monetized by the previous owner.

- Kayak and paddleboard rentals

- Trail access into Sam Houston National Forest

- Firewood bundles, s'mores kits, and welcome packages

- Partner commissions on local fishing, boating, and adventure tours

We’re not inventing anything here — just implementing what already works at Cameron Ranch and comparable operators in the corridor.

Property Improvements

Renovations complete by Month 6, with full stabilization expected by Month 12.

NOI Margin at Stabilization

Margins grow from 51% in Year 1 to 63% at stabilization — well above the 40–50% glamping industry benchmark.

Year 2 Revenue Target

A 39% increase from current trailing revenue, driven by ADR growth, direct booking conversion, and ancillary revenue streams.

Capital Improvement Program

The construction budget is $442K, and every dollar is tied to a specific rate increase or new revenue stream. (The rehab loan is drawn against a $451K basis — the $442K of work plus capitalized financing costs — see Sources & Uses.)

| Sauna, Cold Plunge, Pergola & Outdoor Amenities (×5) | $200,000 |

| Cabin Interior Upgrades (×5) | $74,000 |

| Community Self-Service Kiosk | $35,000 |

| Landscaping (common + individual areas) | $75,000 |

| Contingency (15%) | $58,000 |

| Total Capital Improvements | $442,000 |

Forced Appreciation

| Year 1 NOI (pro forma) | $194,000 |

| Year 1 Value (12% cap) | $1,619,000 |

| Purchase Price | $1,900,000 |

| Stabilized NOI (Year 2) | $342,000 |

| Stabilized Value (12% cap) | $2,848,000 |

| Value Created (over purchase price) | $948,000 |

| Exit Value (Year 10, 10% cap, net of disposition costs) | $3,804,000 |

Revenue Growth Levers

Gross revenue grows from $391K to $544K through three levers, each validated by comparable operators in the market.

| Lever | Current | Target | Impact |

|---|---|---|---|

| Nightly rate (dynamic pricing + amenity premium) | $206 flat | $304 | +$98/night on list rate |

| Direct Booking % (reduce OTA commissions) | 58% | 80% | +22 pts — lower OTA fees |

| Ancillary Revenue (packages, rentals, retail) | $3.6K | $89K | +$85K new revenue |

| Stabilized Revenue (gross) | $391,134 | $543,589 | +39% |

Lever impacts are directional and not strictly additive (rate, occupancy, and channel mix interact). Nightly-rate target benchmarked to Cameron Ranch Glamping ($449–$499 published rates, ~221 SF units — Babia’s $304 target is 32–39% below their published rates for units less than half the size). Ancillary adoption assumes conservative 3% on all discretionary upsells.

Deal Milestones

Q2 2026

Close

Acquisition + begin phased renovation

Q1 2027

Reno Complete

Saunas, plunge pools, kiosk operational

Q3 2027

Stabilized

$304 ADR · $544K revenue · $2.9M value

2029

Refinance

$136K returned to investors · 21% of equity back

2036

Exit

$400K NOI · $3.8M valuation · $2.2M cumulative to investors

Post-renovation rendering: private sauna, cold plunge, expanded deck

10-Year Pro Forma Summary

Annual figures shown below. Year 1 reflects the ramp-up period, Years 2+ are at stabilization, Year 3 includes refinance proceeds, and Year 10 includes exit.

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 7 | Year 10 | |

|---|---|---|---|---|---|---|---|

| Effective Gross Income | $379,903 | $543,589 | $554,460 | $565,550 | $576,861 | $600,166 | $636,901 |

| Operating Expenses | ($185,637) | ($201,836) | ($205,873) | ($209,991) | ($214,190) | ($222,844) | ($236,483) |

| Net Operating Income | $194,266 | $341,752 | $348,587 | $355,559 | $362,670 | $377,322 | $400,417 |

| NOI Margin | 51.1% | 62.9% | 62.9% | 62.9% | 62.9% | 62.9% | 62.9% |

| Investor Cash Flow (operations) | $25,528 | $85,296 | $88,713 | $93,655 | $97,211 | $104,537 | $116,085 |

| Refi / Exit Proceeds | — | — | $136,289 | — | — | — | $1,177,438 |

| Total Investor Cash Flow | $25,528 | $85,296 | $225,002 | $93,655 | $97,211 | $104,537 | $1,293,523 |

Year 3 includes refi proceeds ($136K). Refi at Month 36: 75% LTV. Year 10 includes exit at a 10% cap rate, net of disposition costs. Cumulative investor distributions over 10 years: $2.2M on $650K invested (3.45× MOIC).

Scenario Analysis

These three scenarios stress-test the investment across different revenue and exit cap rate assumptions. Even in the bear case, the deal covers debt service and returns capital.

| Bear Case | Base Case | Bull Case | |

|---|---|---|---|

| Stabilized Revenue | $435K (−20%) | $544K | $598K (+10%) |

| Stabilized NOI | $273K | $342K | $376K |

| Year 2 DSCR | 1.62× | 2.03× | 2.23× |

| Exit Cap Rate | 14% | 10% | 9% |

| Exit Valuation | $2.9M | $3.8M | $4.5M |

| Investor IRR | 12.8% | 19.4% | 25.6% |

| MOIC | 2.3× | 3.45× | 4.7× |

Bear case assumes 20% revenue miss and cap rate expansion. Bull case assumes 10% revenue outperformance and cap rate compression. All scenarios assume the same capital structure and hold period.

Full exit strategy, refi waterfall, and cumulative return detail available in the Appendix.

| Total Equity Raise | $650,000 |

| Minimum Investment | $100,000 |

| Acquisition Fee | 5% of Project Cost |

| Hold Period | 10 Years |

| Target Close | June 1, 2026 |

| Projected IRR | 19.4% |

| Projected MOIC | 3.45× |

| Projected Cash-on-Cash | 14.0% |

Capital Stack

Full sources & uses and financing detail available in the Appendix.

What a $100K investment looks like

Here’s what the projected cash flow looks like on a $100,000 investment. Year 3 includes refinance proceeds and Year 10 includes exit.

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 7 | Year 10 | |

|---|---|---|---|---|---|---|---|

| Annual Cash Flow | $3,927 | $13,119 | $34,608 | $14,405 | $14,952 | $16,079 | $198,958 |

| Cumulative | $3,927 | $17,046 | $51,654 | $66,059 | $81,011 | $112,600 | $345,469 |

Year 3 includes $20,963 refi proceeds. Year 10 includes $79,037 exit proceeds. All figures are projections based on the Official Underwriting model.

Capital Raise

$650K Investor Equity Target

$350K committed · $300K remaining

Co-Sponsors

Gideon Spencer

$9M+ personal hospitality portfolio — 8 hotels invested, 1 operating

The Quad, San Antonio — 31% IRR, 11% Cash-on-Cash (realized)

The Marlo, Solvang — Boutique hotel, owner-operator (operating)

38 hotels across the Incredible Hospitality community, $300M AUM

$23M in student deal volume across 200+ trained investors

Incredible Hospitality Podcast — 86 episodes, 5 stars

Property Operations — Single Seed Stays

Veteran-owned. 15+ years combined experience. 4 properties across Tennessee and New York. 650+ guest families served.

Beau Sydes

Former Head Coach, Cirque du Soleil at Walt Disney World

STR operator — portfolio across multiple markets

SMU graduate, NCAA Division I athlete

Jonas Harper

Full-time hospitality developer and operator

Former Contracts Director, Dept. of Defense — $21B, 35 employees

Marine Corps veteran

MBA in Finance, UMass Lowell

Ellerie Fuller

Former Director of Quality Assurance, Dept. of Defense

Retired Air Force veteran

Maintains 4.95+ star ratings across all properties

MA in Positive Psychology, Life University

Brand, Design & Strategy

Tiffany Zhou

Founded Studio Zhou — vertically integrated design-build

28-unit STR portfolio, seven-figure annual revenue

Leading a $3M, 10-unit ground-up expansion

MFA in Interior Design

Janet Ng

$1.5B in assets overseen across 3.4M SF

Launched 13 dining, wellness, and event venues — $2M annual revenue

51% operational efficiency gains, 4.8/5.0 guest ratings

Houston’s backyard. One of the fastest-growing counties in America.

Montgomery County, TX sits at the intersection of explosive population growth, high household income, and one of the most visited national forests in the state. Stay in Babia is 60 minutes from 7.3 million people looking for a weekend escape.

Drive Times

Competitive Set

| Property | Distance | Units | ADR | Rating | Rev / Unit |

|---|---|---|---|---|---|

| Stay in Babia | — | 5 | $206 | 4.95 | $78K |

| The Retreat at Artesian Lakes | 12 mi | 8 | $275 | 4.9 | — |

| Cameron Ranch Glamping | 46 mi | 5 | $297 blended ($449–$499 published) | 4.9 | $89K |

| Getaway Houston | 45 mi | 40 | $199 | 4.7 | — |

| Piney Woods Cabins | 8 mi | 6 | $185 | 4.5 | — |

Industry Tailwinds

Global glamping market growing at 10.3% CAGR through 2030. A-frames growing at 15.6% annually.

Grand View Research, 2024

Global wellness economy. 82% of Americans say wellness is a top priority. Wellness tourists spend 41% more.

Global Wellness Institute, 2023

of millennials prefer experiential travel. 55% actively seek off-the-beaten-path experiences.

Bloomberg / Booking.com, 2024

Glamping demand among 33-50 age group through 2030. Stay in Babia's core demographic.

Grand View Research, 2025

Full Revenue History (20 Months)

Complete monthly revenue and occupancy from launch (March 2024) through October 2025. The property reached stabilized occupancy within 12 months of opening.

| Month | Revenue | Occupancy | Notes |

|---|---|---|---|

| 2024 — Ramp-Up | |||

| Mar 2024 | $4,800 | 19% | First month open |

| Apr | $13,400 | 12% | |

| May | $9,900 | 22% | |

| Jun | $20,500 | 51% | |

| Jul | $21,400 | 63% | |

| Aug | $17,800 | 55% | |

| Sep | $19,300 | 57% | |

| Oct | $26,200 | 51% | Stabilization begins |

| Nov | $27,600 | 73% | |

| Dec | $27,300 | 75% | |

| 2025 — Stabilized | |||

| Jan 2025 | $32,800 | 87% | |

| Feb | $23,700 | 80% | |

| Mar | $28,900 | 93% | |

| Apr | $30,900 | 96% | |

| May | $30,700 | 94% | |

| Jun | $29,800 | 95% | |

| Jul | $37,700 | 99% | Peak month |

| Aug | $32,100 | 97% | |

| Sep | $27,500 | 89% | |

| Oct | $34,100 | 94% | |

Detailed Financial Performance

Current Operating Performance

| Trailing Revenue (gross of platform fees) | $391,134 |

| Occupancy (trailing 12 mo.) | 89.3% |

| Effective ADR (gross rev. ÷ occupied nights) | $240 |

| Owner’s Advertised Rate (flat, no dynamic pricing) | $206 / night |

| RevPAR (gross rev. ÷ available nights) | $214 |

| Guest Rating | 4.95 / 5.0 |

| Direct Booking % | 58% |

| Going-In Cap Rate (trailing NOI ÷ $1.9M) | 14.0% |

Channel Revenue Mix

| Direct Website | $18,470 / mo (58%) |

| Airbnb | $10,700 / mo (34%) |

| Booking.com | $1,260 / mo (4%) |

| Expedia | $706 / mo (2%) |

| VRBO / HomeAway | $372 / mo (1%) |

| Total Monthly Revenue | $31,880 |

Trailing revenue is gross booking revenue (room rent plus cleaning, pet, and other guest fees) per Lodgify PMS — this is the basis for the $214 revenue-per-available-night figure ($391,134 ÷ 5 cabins ÷ 365 nights) and the $78K-per-cabin figure in the comp set. The owner currently charges a flat $206/night with no weekend, seasonal, or holiday pricing; on a 89.3% occupied base that flat rate plus guest fees realizes an effective ADR of $240. The going-in cap rate of 14.0% is trailing in-place NOI divided by the $1.9M purchase price; the Year 1 pro forma NOI of $194K shown in the cash-flow tables is lower because it adds renovation disruption and the cost of professional management the property does not carry today.

Year-over-Year Growth

| Metric | 2024 (Mar–Dec) | 2025 | Growth |

|---|---|---|---|

| Booking Revenue (calendar year) | $194,252 | $360,453 | +85.6% |

| Advertised Rate (flat) | $175 | $206 | +18% |

| Occupancy | 64.1% | 90.8% | +26.7 pts |

| Rate × Occupancy | $112 | $187 | +67.5% |

Calendar-year booking revenue (2024 covers Mar–Dec, the first ten months of operation). The trailing-12-month figure of $391,134 used elsewhere covers Nov 2024–Oct 2025 and is stated gross of platform fees; the flat advertised rate and Rate × Occupancy figures above are on a room-rate basis.

Cabin-Level Performance (Sep–Oct 2025)

| Cueta | $7,320 / mo |

| Pinos | $6,980 / mo |

| Riolago | $6,960 / mo |

| Torre | $6,410 / mo |

| Huergas | $6,410 / mo |

| Total | $34,080 / mo |

| Cueta | 100% occ. |

| Torre | 97% |

| Riolago | 94% |

| Pinos | 94% |

| Huergas | 84% |

| Average | 94% |

Sources & Uses of Capital

Sources of Capital

| 1st Position — Acquisition (80% LTV) | $1,520,000 |

| 1st Position — Rehab (100%) | $451,360 |

| Investor Equity — Down Payment | $380,000 |

| Investor Equity — Additional at Close | $270,148 |

| Total Sources | $2,621,508 |

Uses of Capital

| Purchase Price | $1,900,000 |

| Rehab & Improvements (incl. capitalized loan costs) | $451,360 |

| Contingency (11.6%) | $52,403 |

| Acquisition Fee (5%) | $96,568 |

| SBA/Lender Fees (2.9%) | $57,930 |

| Closing Costs (1.65%) | $31,350 |

| Working Capital & Reserves | $31,897 |

| Total Uses | $2,621,508 |

Financing Summary

Acquisition & Rehab Loan

| Senior Loan Amount | $1,971,360 |

| Interest Rate | 8.5% |

| Amortization | 25 Years |

| Interest-Only Period | 36 Months |

| Balloon | Month 36 |

Permanent Loan (Refi)

| Refi Timing | Month 36 |

| Interest Rate | 6.5% |

| LTV | 75% |

| Amortization | 25 Years |

| DSCR at Take-Out | 2.11× |

| Net Cash from Refi | $136,289 |

Risk Factors

Every investment carries risk. Here is how we think about and mitigate the key ones.

| Risk | Exposure | Mitigation |

|---|---|---|

| Market Demand | Recession or travel decline | 2.11× DSCR at take-out. Glamping benefits from trade-down spending. |

| Operational | Key person risk, staffing | Documented SOPs, Hospitable automation, local contractor network. |

| Interest Rate | Variable rate increases | 8.5% SBA rate with 2-year I/O period for cash flow cushion. |

| Competition | New glamping entrants | 4.95-star moat. 2× competitor unit size. Forest-adjacent location. |

| Seasonality | Winter demand softness | Sauna/plunge additions. Winter demand index already 107%. |

10-Year Cash Flow Summary

Detailed annual projections for investor cash flow, including distributions, refinance proceeds, and exit.

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 7 | Year 10 | |

|---|---|---|---|---|---|---|---|

| Gross Revenue | $379K | $544K | $554K | $565K | $577K | $600K | $637K |

| Operating Expenses | ($186K) | ($202K) | ($206K) | ($210K) | ($214K) | ($223K) | ($237K) |

| Net Operating Income | $194K | $342K | $349K | $356K | $363K | $377K | $400K |

| Debt Service | ($176K) | ($176K) | ($176K) | ($142K) | ($142K) | ($142K) | ($142K) |

| Investor Distributions | $26K | $85K | $89K | $94K | $97K | $105K | $116K |

| Refi / Exit Proceeds | — | — | $136K | — | — | — | $1,177K |

All figures are projections. Year 3 includes refinance proceeds ($136K). Year 10 includes exit. Cumulative investor distributions: $2.2M (3.45× MOIC).

Key Underwriting Assumptions

- ADR: The owner currently charges a flat $206/night with no dynamic pricing; on the trailing occupied base that flat rate plus cleaning, pet, and other guest fees realizes an effective ADR of ~$240/night. Year 1 underwriting: $240/night. Year 2+ stabilized: $304/night (benchmarked to Cameron Ranch, which publishes $449–$499/night for ~221 SF units — less than half the size of Babia’s 544 SF cabins).

- Occupancy: Year 1: 85% (renovation disruption). Year 2+: 90% (trailing 12-month: 89.3%; trailing 6-month: 94%).

- Revenue Growth: 2% annual escalation after Year 2.

- Operating Expenses: 37.1% of EGI at stabilization. 2% annual escalation.

- Acquisition Financing: 80% LTV, 8.5% rate, 25-year amortization, 3-year balloon.

- Rehab Financing: 100% of the $451K rehab loan basis ($442K construction budget plus capitalized loan costs), interest-only during renovation.

- Refinance: Month 36. 6.5% permanent rate, 75% LTV, 25-year amortization.

- Exit: Year 10 sale at a 10% exit cap rate; ~$3.8M net of disposition costs (before debt payoff).

- Ancillary Revenue: $89K total ($17.8K/unit) at stabilization. 3% adoption on discretionary upsells.

- Direct Booking Target: 80% by Year 2 (currently 58%).

Exit Strategy & Investor Return Waterfall

Year 10 exit. Multiple liquidity paths. 21% of equity returned at refinance.

Refinance (Year 3)

| Timing | Month 36 (0% prepay penalty) |

| Terms | 6.5% rate, 75% LTV, 25-yr am |

| Net Refi Proceeds to Investors | $136,289 |

| % of Equity Returned | 21% |

Sale (Year 10)

| Year 10 NOI | $400,417 |

| Net Sale Proceeds | $3,804,000 |

| Less: Loan Payoff | ($1,969,872) |

| Net to Equity | $1,834,092 |

| Investor Share (Year 10) | $1,293,523 |

Cumulative Investor Returns

| Total Investor Equity Invested | $650,148 |

| Cumulative Operating Distributions (10 yrs) | $932,536 |

| Refi Proceeds (Year 3) | $136,289 |

| Exit Proceeds (Year 10) | $1,177,438 |

| Total Investor Distributions | $2,246,059 |

| MOIC | 3.45× |

Exit Paths

Operator Sale

Glamping operators acquiring stabilized properties with strong reviews and direct booking infrastructure. 4.95 stars and 600+ reviews are high-value acquisition assets.

Portfolio Buyer

Institutional capital entering the glamping space. A 5-unit property with 60%+ NOI margins is an attractive bolt-on for a regional portfolio.

Self-Service Camp Store & Ancillary Revenue

A self-service kiosk and camp store is a core component of the $442K renovation plan. The model is benchmarked to Cameron Ranch Glamping, which operates a similar program at $6,000 per cabin annually. This is a proven revenue stream in glamping that requires no staffing — guests purchase on an honor system or via automated payment.

Projected Ancillary Revenue Streams

| Revenue Stream | Per Cabin | Total (5 Cabins) | Notes |

|---|---|---|---|

| Vending / Camp Store | $6,000 | $30,000 | Cameron Ranch benchmark |

| Premium Spa Package ($75) | $435 | $2,175 | 3% adoption × 976 bookings |

| Sauna Add-On ($40) | $234 | $1,170 | 3% adoption |

| Firewood Bundles ($20) | $1,952 | $9,760 | 50% adoption (passive purchase) |

| Pet Fees ($75) | $1,464 | $7,320 | 10% of stays |

| Branded T-Shirts ($35) | $203 | $1,015 | 3% adoption |

| Early Check-in ($50) | $290 | $1,450 | 3% adoption |

| Late Check-out ($50) | $290 | $1,450 | 3% adoption |

| Kayak / Paddleboard Rentals ($50) | $976 | $4,880 | 10% adoption, seasonal |

| Welcome Packages ($35) | $203 | $1,015 | 3% adoption |

| Rebooking Credit ($50) | $2,928 | $14,640 | 15% adoption — retention driver |

| Total Ancillary Revenue | $17,818 | $89,090 | +2,406% vs. current ($3,555) |

Assumptions: 976 bookings/year (2025 actual). Pet fee at $75 (below Cameron Ranch's $100). Conservative 3% adoption on all discretionary upsells. Vending/retail benchmarked to Cameron Ranch at $6,000/cabin. Rebooking credit modeled after Cameron Ranch's $50 rebooking program — costs nothing upfront, drives repeat visits.

Cameron Ranch Benchmark

Cameron Ranch Glamping (Coldspring, TX — 46 miles from Stay in Babia) provides the most direct validation for this ancillary revenue model. Key comparisons:

| Cameron Ranch | Stay in Babia (Target) | |

|---|---|---|

| Units | 5 (3 glamping + 2 houses) | 5 |

| Unit Size | ~221 SF (mirror house, domes, cabins) | 544 SF (A-frame cabins) |

| ADR (Published) | $449 weekday / $499 weekend | $304 (post-renovation) |

| ADR (Blended) | $297 | $304 (post-renovation) |

| $/SF/Night | $1.34–$2.26 | $0.56 |

| Rev / Unit | ~$89K/unit (~$12K/mo on flagship) | $109,000/unit |

| Ancillary Rev / Unit | — | $17,818/unit |

| Camp Store / Unit | $6,000/unit | $6,000/unit (benchmarked) |

| Experience Packages | $50 rebooking, $100 pet fee, spa packages | $50 rebooking, $75 pet fee, spa & sauna packages |

| Guest Rating | 4.9 ☆ | 4.95 ☆ |

Source: AirDNA, Cameron Ranch Glamping website, operator data. Cameron Ranch validates that premium glamping guests actively embrace upsells when the experience justifies the pricing.

Disclaimer & Confidentiality

The information contained in this Investment Overview has been prepared by Stonemont Capital. All financial projections, financial information, pro forma statements, and other information are only estimates of potential revenues, expenses, cash flow, and profit and losses. The financial information does not constitute projections of investment returns.

The enclosed information does not constitute an offer to sell an interest in the Limited Partnership. A purchase of an interest can only be undertaken as expressly set forth in the Limited Partnership Agreement, Subscription Agreement, and Private Placement Memorandum.

This document is private and confidential. Past performance is no guarantee of future results. This document may not be copied, reproduced, or transmitted without prior written consent of the Partners.

Get in Touch

Ready to discuss this opportunity? Reach out directly.